Érica Missão

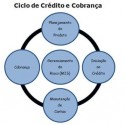

The Credit and Debt Collection Cycle is present in almost all sectors of the industry as banking, retail, telecommunication etc. It is typically divided into five fundamental stages, as described below.

The first stage of the Credit and Debt Collection is the product planning, stage where the target public is determined as well as the characteristics of the product, the acceptance of risk associated to the product and its profitability. The second stage is concerned with granting consumer credit, it may be a bank loan, an installment purchase contract or even the purchase of a phone line. Account management is the stage where it is observed the relation between the customer behavior and the credit granted. In this stage it is also possible to identify some opportunities, as offering new products, increasing credit, calculating debt risk etc. Debt Collection is the stage where the debt risk has already achieved 100%, because the customer is no longer a non-debtor, and it is time to focus on maximizing revenue and minimizing financial losses. A Management Information System (MIS) – is the centerpiece of this cycle where numbers are processed into information through historical data so that decision-making becomes more assertive.

A crucial question is “How to work at every stage of the credit and debt collection cycle to reduce risks?”

Currently there are several methodologies used in the industry leading to results in the short, medium and long term. The purpose of this post is to illustrate the use of statistical tools.

At the stage of product planning a good suggestion is to start with market research (benchmarking – process of determining who is the very best), i.e. evaluating the success of the product (including both sales and payments). It is important to note that despite the research been made to mitigate the risk, it still exists and should be considered in the process.

In the stage of granting consumer credit is essential to establish an accurate credit policy. At this time there is insufficient information about the consumer so a common suggestion is to use a technique called “Credit Score” – a statistical model which through an associated score (ranking) indicates the probability of a customer becoming a debtor after the granting of credit. In the step of granting the credit, the Credit Score model helps in the reduction of financial losses, along with other internal company policies. These models can be developed using registration information, trade payment information, public record history etc, the greater the range of data sources, the greater the likelihood they will become robust models.

The third stage, account management, is the time to develop a risk management strategy for the portfolio. At this stage, there is a lot more information regarding the customer behavior and it is possible to measure the risk with greater assertiveness. Considering this point, a suggestion is to use the statistical model called “Behavior Score”. As the name implies, it is a model developed based on behavioral variables (criteria or parameters for measuring and comparing among different individuals) taken from the customer history. The Behavior Score, as well as the Credit Score generates a ranking that indicates the risk of a customer becoming a debtor. The Behavior Score tends to be more robust than the Credit Score because the variables belong to the company’s own portfolio. There is the possibility of using the credit model as a predictive variable in the development of the Behavior Score model and also credit information used in building the Credit Score model.

A statistical technique suggested for debt collection is “Collection Score” and “Self-Cure”, both of which are statistical models focusing on this area, aiming to maximizing revenue, minimizing financial losses and reduce costs. The Collection Score indicates what the probability the consumer pays off a debt, classifying it into low risk, medium risk e high risk. The Self-Cure model shows what is the probability that the consumer will pay his or her debt spontaneously, working well in the early stages of aging debt. The joint use of both models usually provide excellent results because it directs to the area where it is necessary to assign collection efforts and also where there is no need to do so resulting in a highly structured collection policy in addition of being more cost effective. Generally, the Champion and Challenger methodology is used at this stage to assess what is the best payback over the level of risk and debt collection action (such as Voice, SMS – short message service, mail, debt collection letter, virtual assistant etc).

The center point cycle known as MIS – Management Information System – it is the stage that subsidizes the remaining stages, because it is where important historic information is found at each stage of the cycle of credit and debt collection to support the decision making process. There are statistical software packages that also serve to manage entire portfolio risk within the framework structure (MIS). One is the SAS – Statistical Analysis System – an integrated application that allows data recovery; file management, database access, graphs and reports generation and also statistical analysis. This software can be installed on different operating systems available in the industry. The use of this tool, which offers various benefits and advantages, provides complete control over the portfolio risk management through quality information, resulting in a safe analysis environment and therefore a sound decision making process. The information quality is extremely important, because an analysis with inconsistent information may cause irreversible effects on the risk linked to each stage of the credit cycle, affecting the Company’s financial results. However, one can say the Management Information System (MIS) is the key step to the success of any cycle of credit and debt collection.

The use of statistical methods throughout the credit cycle helps considerably in reducing risks at all stages due to the predictive power of the statistical science. Certainly, there are others contributing factors to risk reduction as a having credit and debt collection well defined policy, synergy between goals (credit & debt collection) and data reliability – the last is the most important throughout the entire process.

SUBSCRIBE on Blog Telemarketing and Collection (Blog Televendas & Cobrança in Portuguese) and receive weekly newsletter with our main articles, jobs and breaking news.

Gostou deste artigo? Compartilhe!

Revista Digital

Siga-nos no twitter

Enquete

Categorias

- Atendimento Online (453)

- Call Center (5871)

- Capacity Planning (3)

- Chatbot (104)

- Cliente Oculto (19)

- Cobrança (2912)

- Comunicado (27)

- Concessão de Crédito (4)

- Contact Center (298)

- Crédito (9408)

- Cursos e Eventos (241)

- Dimensionamento (9)

- Discador e Discagem (85)

- Do Not Call List (22)

- Dúvidas dos Leitores (10)

- Educação (51)

- Enriquecimento Cadastral (341)

- Enriquecimento de Dados Cadastrais (48)

- Entrevista (38)

- Estratégia e Modelagem (230)

- Fidelização (265)

- Financeiro (127)

- Fraude (61)

- Gestão (4122)

- Gravações (29)

- Higienização Cadastral (3)

- Indicadores (12)

- Mailing (8)

- Mailing Segmentado (7)

- Meios de Pagamento (95)

- MIS (33)

- Monitoria (8)

- Normas (231)

- Notícias (1998)

- Opinião (617)

- Qualidade (919)

- Redes Sociais (445)

- Sem categoria (5)

- Serasa Experian (1)

- Serviço (3)

- SMS/Voice/Boletos/Email (420)

- Sorteio (8)

- Sustentabilidade (1)

- Tecnologia e Telecom (572)

- Telefone Hot (1)

- Televendas (2880)

- Tendências (2)

- Treinamento (38)

- Vagas (695)

- Vendas (1540)

- Workforce Management (30)

Sobre o Blog

Blog Televendas & Cobrança é o primeiro portal independente do Brasil voltado para estes dois importantíssimos segmentos do setor (Televendas / Cobrança – Telecobrança).

A qualidade dos serviços e a ampla quantidade de informações exclusivas sobre Cobrança, Telecobrança, Televendas, Telemarketing, Vendas, Contact Center, Call Center, Atendimento ao Cliente, SAC disponibilizadas diariamente atraem um público qualificado formado em sua maioria por executivos decisores pela avaliação ou aquisição de ferramentas/produtos ou serviços de nossos anunciantes.